CATL optimistic about US expansion| Chile’s salt flats ready for private tenders

CATL optimistic about US expansion| Chile’s salt flats ready for private tenders

Weekly mining & batteries updates (Mar 25 - 31)

What’s big this week?

1. Mining/minerals: Chile plans tender for salt flats; US seabed disputes; Indonesia expands nickel production despite price plunge.

2. Batteries/EVs: CATL optimistic about US expansion but not solid-state battery; China's battery cell pipeline growth slows.

Starting this week’s update with an interesting quote from CATL’s CEO, Yuqun Zeng:

“Geopolitics is a very transitory issue. Each government administration only lasts four or five years, but business relationships last for decades.”

Zeng also believes that CATL's technologies are unlikely to be caught up in a broader tech war, as governments worldwide all focus on tackling climate change.

Sadly, this hasn’t been the case for CATL's latest battery plant announcement with Ford in Michigan last February. The $3.5 billion battery plant is fully owned and operated by Ford, albeit with technology licensing from CATL. It has faced strong backlash and local protests. Republicans have been scrutinizing Ford's partnership with CATL, fearing the flow of U.S. tax subsidies to China and potential dependence on Chinese technology.

Zeng says that its US expansion would be mainly focusing on technology licensing and is also currently in talks with Tesla.

Zeng also raised doubts about the immediate commercialization of solid-state batteries. The market is buzzing with excitement over solid-state batteries, which eliminate liquid electrolytes and promise a greater driving range. Zeng's comment comes at an interesting time as Toyota has been particularly vocal about its progress in aiming to introduce solid-state batteries as early as 2027.

Mining/ Minerals

Chile provides further details on its lithium nationalization plan with a tender process for 26 salt flats set to begin in April for private investors. The tender is anticipated to conclude in July.

Chile's lithium nationalization plan calls for public-private partnerships in future projects, with state firms leading in the most promising areas, while private firms can dominate in less strategic zones. Chile aims to boost local battery metal production by 70% over the next decade.

Atacama and Maricunga, representing 64% of global reserves, are reserved for state-controlled partnerships.

-

The US faces pushback to its claims of an extended seabed area due to Washington's failure to ratify the United Nations Convention on the Law of the Sea (UNCLOS), a treaty governing access to resources in international waters.

Why hasn’t the US ratified UNCLOS? A CFR analysis points out that this is because of concerns among conservatives about the potential loss of sovereignty to the United Nations. They argued it could give global bureaucrats power over U.S. naval operations and require companies to pay royalties to the International Seabed Authority. The Reagan administration also feared lawsuits over environmental standards for the high seas if the US joined UNCLOS.

-

Indonesia plans to expand nickel output despite low global prices, furthering a supply surge that is expected to wipe out more rivals in the near future.

Due to the glut of supply from Indonesia, more than half of global nickel production is unprofitable at current prices of about $16,500 per tonne. Indonesia's deputy coordinating minister for investment and mining projected long-term nickel prices would be between $18,000 and $19,000.

Production capacity for battery-grade nickel is set to quadruple to 1 million tonnes by 2030, while nickel pig iron capacity is expected to increase by up to 15% in three years.

-

Tsingshan’s battery unit plans to build a battery factory in Indonesia, expected to start operating next year. The ex-China buildout is part of Chinese companies' efforts to mitigate concerns about trade conflicts that threaten exports from China.

-

Chinese copper smelters plan for an output cut of 5-10% this year. China is the world's largest copper producer, accounting for over half of the world's supply. This decision comes as tightening ore supplies has pushed processing fees to nearly zero.

Batteries/ EVs

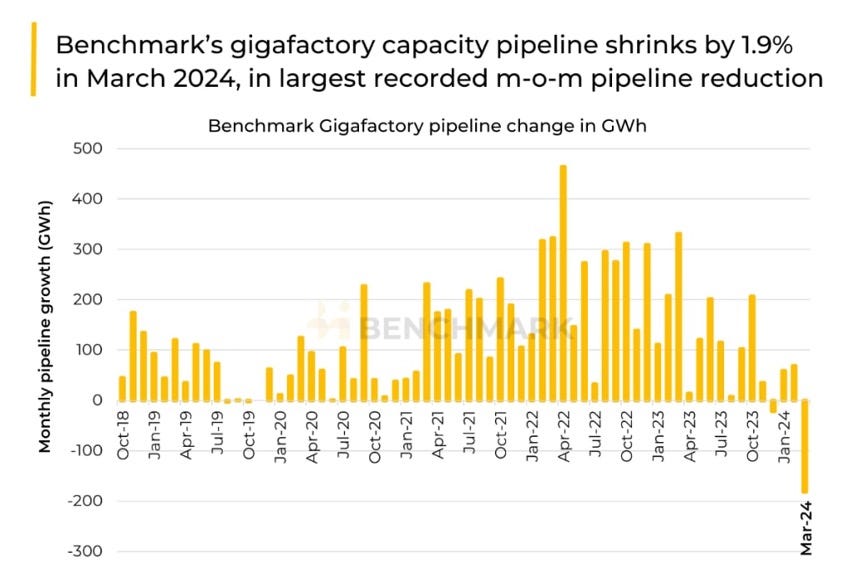

China's battery cell pipeline experienced slower growth in March, marked by reduced capacity and fewer gigafactories. This contraction reflects decreased investment due to a slowdown in EV demand growth and a shift in focus among cell makers toward expanding existing projects. In 2024, larger battery cell producers are expected to outpace smaller ones, signaling a trend toward consolidation in the industry.

-

POSCO inked deals with two unnamed American and European automakers to supply ex-China REPMs. This entails a $680 million deal with a North American automaker from 2026 to 2031, and a $196 million agreement with a European automaker from 2025 to 2034. POSCO will obtain ores and chemicals from Vietnam, the US, and Australia, which are projected to yield 19% of the global mined Praseodymium-Neodymium (PrNd) supply in 2024. The magnets will be produced by Star Group, a South Korean REPM specialist.

If you enjoy our weekly doses of mineral news, please share it with people around you who may also like it -

If you have not yet subscribed to us, oh well here you go -